Heritage Global Inc.'s (NASDAQ:HGBL) Share Price Matching Investor Opinion

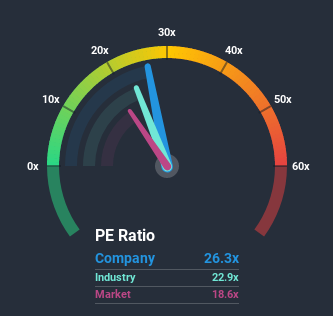

Heritage Global Inc.'s (NASDAQ:HGBL) price-to-earnings (or "P/E") ratio of 26.3x might make it look like a sell right now compared to the market in the United States, where around half of the companies have P/E ratios below 18x and even P/E's below 10x are quite common. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's lofty.

With its earnings growth in positive territory compared to the declining earnings of most other companies, Heritage Global has been doing quite well of late. The P/E is probably high because investors think the company will continue to navigate the broader market headwinds better than most. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

See our latest analysis for Heritage Global

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Heritage Global.

Does Growth Match The High P/E?

In order to justify its P/E ratio, Heritage Global would need to produce impressive growth in excess of the market.

Taking a look back first, we see that the company grew earnings per share by an impressive 34% last year. Still, EPS has barely risen at all from three years ago in total, which is not ideal. So it appears to us that the company has had a mixed result in terms of growing earnings over that time.

Looking ahead now, EPS is anticipated to climb by 125% during the coming year according to the only analyst following the company. Meanwhile, the rest of the market is forecast to only expand by 4.9%, which is noticeably less attractive.

In light of this, it's understandable that Heritage Global's P/E sits above the majority of other companies. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

The Bottom Line On Heritage Global's P/E

Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

As we suspected, our examination of Heritage Global's analyst forecasts revealed that its superior earnings outlook is contributing to its high P/E. At this stage investors feel the potential for a deterioration in earnings isn't great enough to justify a lower P/E ratio. Unless these conditions change, they will continue to provide strong support to the share price.

Before you take the next step, you should know about the 2 warning signs for Heritage Global (1 shouldn't be ignored!) that we have uncovered.

Of course, you might also be able to find a better stock than Heritage Global. So you may wish to see this free collection of other companies that sit on P/E's below 20x and have grown earnings strongly.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.