OBR: UK faces worst downturn in 300 years

The Office for Budget Responsibility (OBR) has revised up the cost of the government’s COVID-19 response by tens of billions and said it expects the UK economy to face its worst downturn in 300 years this year.

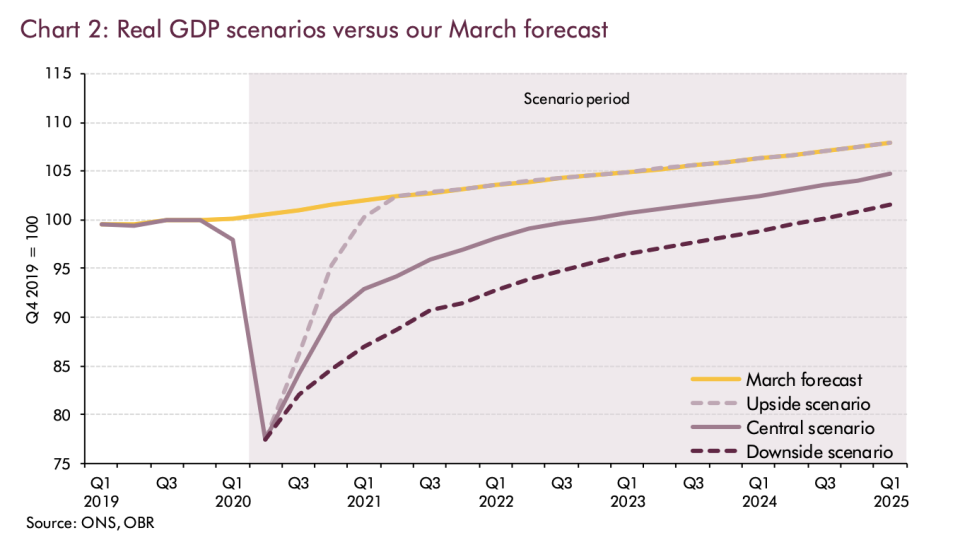

The OBR on Tuesday set out three “scenarios” for the path of the UK economy this year as part of its monthly update on the sustainability of UK public finances.

It’s central, or base, case assumes GDP falls by 12.4% this year with “some potential scarring” to the economy — an economic term for permanently lost output caused by firms going bust or people losing work. Unemployment is forecast to peak at 11.9% in the fourth quarter of 2020.

READ MORE: UK economy shrinks by one-fifth under coronavirus lockdown

The watchdog’s best case scenario still sees GDP fall by 10.6% this year and unemployment peak at 9.7%. In the worse case, economic output could shrink by 14.3% and unemployment could climb to 13.2%.

“The UK is on track to record the largest decline in annual GDP for 300 years, with output falling by more than 10% in 2020 in all three scenarios (and contracting by a quarter between February and April),” the OBR wrote.

Activity is expected to rebound by 8.7% next year but remain below where it was prior to the pandemic for at least the next 5 years.

The government spending watchdog said the cost of tackling the crisis would lead to an “unprecedented” rise in state borrowing to £322bn ($404bn) this year. In May, the OBR said borrowing was likely to be £298bn in 2020.

The increased borrowing forecast came as the OBR also increased its estimate for the cost of the government’s response to COVID-19. The watchdog expected the Treasury to spend £192.3bn this year tackling the pandemic, up from a previous estimate of £132bn.

The update partly reflects new spending pledges announced by the chancellor Rishi Sunak at his “mini-budget” last week. The chancellor announced stimulus worth £30bn to kickstart an economic recovery and revealed that the government had already spent £160bn supporting the economy and the health service.

READ MORE: UK chancellor unveils £30bn plan to protect millions of jobs

Last month UK debt passed 100% of GDP for the first time since 1963 and the government broke records for monthly borrowing.

The OBR said that while the government was rightly focused on limiting the damage of the pandemic, it would eventually have to tackle the sky-high debt and budget deficits.

“It seems likely that there will be a need to raise tax revenues and/or reduce spending (as a share of national income) to put the public finances on a sustainable path,” the OBR said.

The OBR was set up by former chancellor George Osborne in 2010 to provide an independent audit of public finances, with a focus on the sustainability and affordability of debt.